What is the best money budget rule?

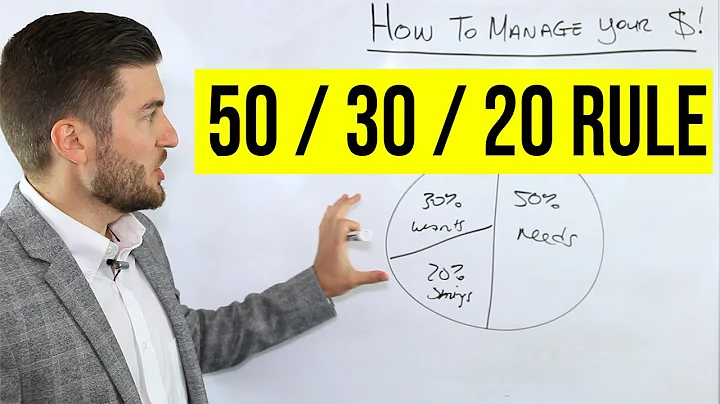

The 50/30/20 budget rule states that you should spend up to 50% of your after-tax income on needs and obligations that you must have or must do. The remaining half should be split between savings and debt repayment (20%) and everything else that you might want (30%).

In the 50/20/30 budget, 50% of your net income should go to your needs, 20% should go to savings, and 30% should go to your wants. If you've read the Essentials of Budgeting, you're already familiar with the idea of wants and needs.

Oh My Dollar! From the radio vaults, we bring you a short episode about the #1 most important thing in your budget: your values. You can't avoid looking at your budget without considering your values – no one else's budget will work for you.

The 50/30/20 budget can be a simple and effective way to structure your finances. To get started, review your financial situation and goals, and come up with a formula that works for you. Whatever budgeting method you choose, it will only work if you stick to it.

The 50-30-20 rule recommends putting 50% of your money toward needs, 30% toward wants, and 20% toward savings.

Key Points. The 50-30-20 rule is a simple guideline (not a hard-and-fast rule) for building a budget. The plan allocates 50% of your income to necessities, 30% toward entertainment and “fun,” and 20% toward savings and debt reduction.

CBO: U.S. Federal spending and revenue components for fiscal year 2023. Major expenditure categories are healthcare, Social Security, and defense; income and payroll taxes are the primary revenue sources.

To save that amount of money in a year, you would need to earn a very high income and have an extremely low cost of living. For example, if you wanted to save $200,000 in a year, you would need to save an average of over $16,000 per month. If you assume a 30-day month, that's over $500 per day.

- Financial Goals Aren't Clear. ...

- Not Tracking Expenses. ...

- Overspending. ...

- Not Planning For Unexpected Expenses. ...

- Not Adjusting Budgets As Circ*mstances Change. ...

- Thinking That Budgeting Is Easy. ...

- Underestimating Expenses. ...

- Relying Too Much On Credit.

The 70-20-10 budget formula divides your after-tax income into three buckets: 70% for living expenses, 20% for savings and debt, and 10% for additional savings and donations. By allocating your available income into these three distinct categories, you can better manage your money on a daily basis.

Can you live off $1,000 a month after bills?

Bottom Line. Living on $1,000 per month is a challenge. From the high costs of housing, transportation and food, plus trying to keep your bills to a minimum, it would be difficult for anyone living alone to make this work. But with some creativity, roommates and strategy, you might be able to pull it off.

The 30% Rule Is Outdated

To start, averages, by definition, do not take into account the huge variations in what individuals do. Second, the financial obligations of today are vastly different than they were when the 30% rule was created.

“Saving $20,000 per year is about $1,667 per month or about $385 per week,” she said. “Thinking about it in smaller terms makes it less daunting of a goal.”

“Your most powerful wealth-building tool is your income. And when you spend your whole life sending loan payments to banks and credit card companies, you end up with less money to save and invest for your future.

Savings by age 30: the equivalent of your annual salary saved; if you earn $55,000 per year, by your 30th birthday you should have $55,000 saved. Savings by age 40: three times your income. Savings by age 50: six times your income.

The 50/30/20 budget rule states that you should spend up to 50% of your after-tax income on needs and obligations that you must have or must do. The remaining half should be split between savings and debt repayment (20%) and everything else that you might want (30%).

The 40/40/20 rule comes in during the saving phase of his wealth creation formula. Cardone says that from your gross income, 40% should be set aside for taxes, 40% should be saved, and you should live off of the remaining 20%.

The 20/10 rule follows the logic that no more than 20% of your annual net income should be spent on consumer debt and no more than 10% of your monthly net income should be used to pay debt repayments.

In 2023, major entitlement programs—Social Security, Medicare, Medicaid, Obamacare, and other health care programs—consumed 50 percent of all federal spending. Soon, this spending will be larger than the portion of spending for all other priorities (such as national defense) combined.

The main source of income in Union budget

Personal income tax and taxes on profit of private companies are the main direct taxes. They also include capital gains tax and wealth tax. The GST (the Centre's share in it) is an indirect tax. Then there are excise and customs duties collected by the Union government.

What does the government spend the most money on?

Nearly half of mandatory spending in 2022 was for Social Security and other income support programs such as the Child Tax Credit, food and nutrition assistance, and federal employee benefits (figure 3). Most of the remainder paid for the two major government health programs, Medicare and Medicaid.

When your savings reaches $100,000, that's a milestone worth marking. In a world where 57% of Americans can't cover an unexpected $1,000 expense, having a six-figure savings account is commendable.

A great way to grow 100K into a million is through a diversified investment portfolio. This can include exchange-traded funds (ETFs) for broad market exposure, dividend stocks for steady income, and growth stocks for higher potential returns.

“By the time you're 40, you should have three times your annual salary saved. Based on the median income for Americans in this age bracket, $100K between 25-30 years old is pretty good; but you would need to increase your savings to reach your age 40 benchmark.”

Essentially, any income that isn't permanent should not be included in your main budget. I know for a lot of us it is instinctual to see money and say “Oh look! I have more money to spend!” But I encourage you to take a step back and only plan for what income that comes in regularly.